2026 is shaping up to be a year defined by cautious economic growth and rapid structural change.

Demand in the US and Europe is still soft, inflation is cooling, and PMIs are hovering around the no-growth line. But at the same time, global trade is expanding, developing economies are driving more of the world’s industrial output, and technology investment, particularly AI, is accelerating faster than any other period in the past decade.

So instead of one single story shaping 2026, we’re entering a year where each region, sector, and supply chain is moving at its own pace. This is a breakdown of the 11 trends that matter most, and what they actually mean for manufacturers navigating this mixed environment.

1. 2026 Opens on Shallow, Cautious Growth

If we zoom out across the last 12 months of PMI data, the Eurozone is sending one clear signal: the industrial economy is stuck in a slow-moving loop.

The Eurozone’s PMI dipped below 50 earlier in 2025, then recovered to 51.2 by September, according to S&P Global. It technically signals expansion, but the growth is so small that it translates to only about a 0.2% increase in GDP.

In the US, the ISM Manufacturing PMI came in at 49.1, which means the sector is still shrinking, new orders fell again, exports dropped sharply, and companies are continuing to cut jobs.

Manufacturing exports are also slipping again because companies are no longer rushing orders ahead of US tariffs, which means the temporary boost from earlier this year has disappeared.

What this means for 2026 is straightforward: the global recovery is likely to stay slow unless consumers and businesses start spending again. Manufacturers in both the US and EU are producing more carefully, managing headcount, and keeping inventories tight because they aren’t sure if orders will grow.

And PMI trends show that until demand strengthens, 2026 will likely be a year of cautious, uneven growth in manufacturing across both economies.

2. Global Trade Surges Ahead Despite Weak PMI Signals

Despite weak PMI signals in the US and eurozone, global trade itself is proving far more resilient. According to UNCTAD’s Global Trade Update published in October 2025, global trade expanded by about $500 billion in the first half of 2025, with goods trade growing 2.5% and services accelerating sharply into Q3.

Even with tariff turbulence and geopolitical uncertainty, UNCTAD expects 2025 to set a new record for global trade, meaning that while regional manufacturing surveys look weak, the overall global trading system is still expanding and manufacturers with diversified global footprints will benefit the most in 2026.

3. Geopolitics Becomes a Core Variable in Production Planning

Regional conflicts are no longer background risks. They are now direct variables in production, costing, and inventory decisions.

According to the 2025 Fictiv State of Manufacturing Report, 91% of manufacturing leaders now factor global tensions (Ukraine, Middle East, Red Sea disruptions) into long-term supply chain planning. And 93% believe that this will escalate in the next few years. For instance, the Red Sea crisis alone has increased shipping costs from Asia to Europe by more than 5 times.

As a result, companies are placing inventory closer to customers, diversifying production, and building more redundancy into supply chains, not temporarily, but as part of a long-term strategy.

4. Neutral Manufacturing Hubs Gain Momentum

As tariff volatility increases, manufacturers are seeking “neutral” countries that sit outside major trade conflicts. India, Mexico, and Switzerland continue to gain traction.

For example, Apple exported $10B worth of iPhones from India in FY26 H1, accounting for 20% of global sales. But it’s not just Big Tech making this move. In May 2025, Foxconn announced a US$1.5 billion expansion of its Indian operations to deepen its manufacturing footprint and reduce China exposure. And MGA Entertainment, which primarily had its manufacturing hub in China, has planned to move 40% of its manufacturing to India, Vietnam, and Indonesia within six or so months.

In 2026, more companies are expected to distribute production across multiple politically neutral regions to reduce exposure to tariff and regulatory swings.

5. Climate Finance Accelerates After COP30, but Fossil Policy Splits Remain

COP30 conducted recently in Brazil ended with a deal that reveals the two-speed reality shaping global climate and trade policy in 2026.

On one hand, wealthy nations have agreed to triple climate-adaptation finance for developing countries by 2035. But despite this progress, COP30 avoided any mention of fossil fuels, after major producers such as Saudi Arabia blocked language calling for a phase-down.

This creates a defining trend for 2026: climate finance will accelerate, but fossil-fuel policy will fracture.

Manufacturers should expect the following next year:

- We can expect stricter reporting and compliance from global suppliers, especially in agriculture, mining, apparel, and energy-intensive manufacturing.

- COP30 initiated a formal process to review how global trade frameworks can align with climate objectives. This means green trade rules (like the EU’s CBAM) will become part of standard supply-chain compliance.

- Fossil exporters will continue doubling down on oil and gas investments, while climate-vulnerable countries will fast-track renewables and demand cleaner supply chains from their trade partners.

With the United States absent from COP30, leadership is decentralizing, giving blocs such as the EU, Latin America, and small island states greater influence over climate-trade alignment.

6. Tariffs Become a Fixed Cost Factor

Tariffs are no longer a temporary shock; they’re becoming a predictable cost line on every manufacturer’s balance sheet. WTO modeling shows global goods trade could fall 0.2% in 2025, and as much as 1.5% under more severe tariff regimes. Meanwhile, the National Association of Manufacturers reports that more than half of US manufacturers are now paying over $250K in annual tariffs, with nearly a third paying more than $1M.

The era of waiting for tariff clarity is over. Entering 2026, most global manufacturers will plan with tariffs baked directly into pricing, sourcing, and margin calculations rather than treating them as exceptions.

7. Multi-Shoring Replaces Friendshoring Altogether

UNCTAD data shows that the friendshoring wave of 2022–2023 has now fully plateaued. Throughout 2025, companies moved decisively toward multi-shoring, spreading production across India, Poland, Vietnam, Mexico, and other neutral or low-risk regions instead of relying on one aligned “bloc.”

The old model of a single primary manufacturing base supported by peripheral suppliers is weakening; companies are instead constructing layered, parallel production footprints. And this pattern of multi-shoring is expected to increase in 2026, where having flexible production locations becomes the competitive edge.

8. AI’s Role Expands From Factory Efficiency to Full Value-Chain Intelligence

Many global manufacturers have started using artificial intelligence as a part of their production line to make create smarter solutions. In fact, the Deloitte 2026 Manufacturing Outlook report, found that 80% of manufacturing executives plan to invest 20% or more of their budgets in smart manufacturing initiatives.

And 56% of manufacturers have already noticed a cost reduction using AI, according to McKinsey’s report on The State of AI in 2025. For instance, Bosch committed €2.5B to AI innovation by 2027, explicitly targeting factory performance.

Many manufacturers are also investing in robotic dogs and humanoid robots to work in unstructured areas like production units, with 22% of manufacturers planning to use robots in the next two years. Among the countries investing in industrial robots, China tops the list with 295,000 industrial robots installed in 2024, nearly 10× the US, while US installations fell 9%. UBS forecasts annual sales of humanoids reaching 1 million by the 2030s.

But AI isn’t just being used in the production lines. 2026 is expected to mark the first major shift toward AI-driven, autonomous aftermarket operations. Manufacturers are now deploying agentic AI systems that can independently detect component wear, schedule service calls, order replacement parts, reroute inventory, and even triage warranty claims, all with human approval loops.

In 2026, AI won’t just support production tasks. It will increasingly become a vital part of managing planning, maintenance, aftermarket operations, quality control, and supply-chain decision-making in real time.

9. CBAM Becomes Standard Compliance

The EU’s Carbon Border Adjustment Mechanism (CBAM) begins full enforcement in Jan 2026, requiring importers to buy CBAM carbon certificates for steel, aluminium, cement, fertilisers, and more.

CBAM marks the start of carbon becoming a “costed” input in global manufacturing. In 2026, companies will no longer track emissions for reporting. They’ll track them because carbon intensity will directly shape sourcing, pricing, and trade competitiveness across every major supply chain.

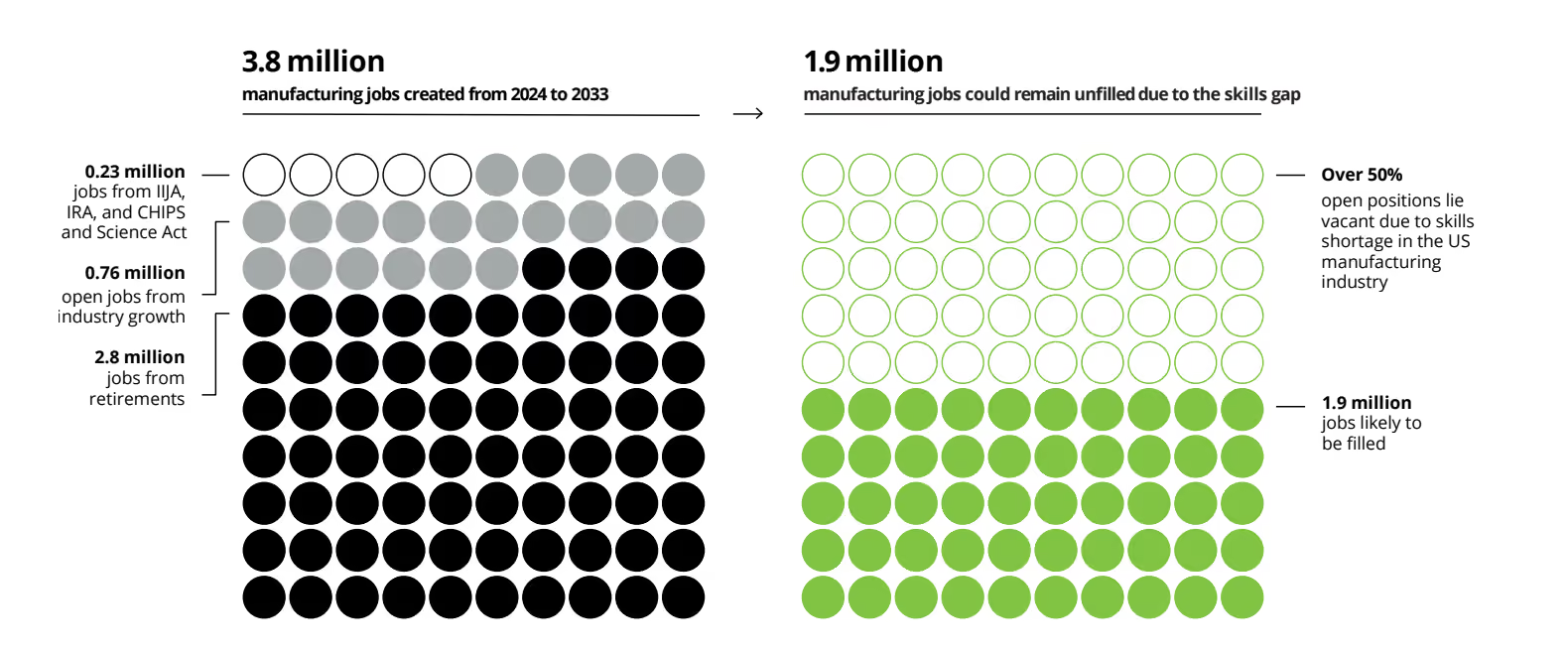

10. Workforce Gaps Widen Despite Rising Demand for Skilled Roles

A report by Deloitte and The Manufacturing Institute estimates that 3.8 million new manufacturing jobs will be needed between 2024 and 2033, but nearly half of them (1.9 million) could go unfilled.

The report shows that the next decade will favour high-skill, tech-enabled role, from maintenance technicians (projected to grow 16%) to mechanical/industrial engineers (+11%) and software & data-driven roles (+13%). Even niche positions like manufacturing data scientists may expand by almost 30%, signalling that analytics and digital fluency will be as critical as traditional machining or assembly skills.

11. Rare Earths Become a Front-Line Strategic Issue

Rare earths are no longer a quiet supply-chain dependency sitting in the background of electronics, EVs, batteries, and defense systems. In 2026, they will become one of the most important global manufacturing risk factors to watch. China still controls over 90% of global rare-earth processing. Although the US, EU, India, Australia, and Japan are all accelerating diversification, it takes an average of 16.5 years for a new mine to move from discovery to first production.

At the same time, demand is climbing sharply: the IEA projects a three- to seven-fold increase in rare-earth needs by 2040, driven primarily by EV motors, wind turbines, and high-performance electronics. And with the US announcing new measures to reduce its dependence on Chinese supply, the geopolitical tension around these minerals will likely intensify rather than ease.

In 2026, manufacturers need to watch out for supply-chain concentration risks, price spikes in neodymium and dysprosium, new long-term agreements from automakers, and the first signs of competitive bidding between the US and China for processing capacity.

.svg)