The U.S. trade landscape has shifted sharply in 2025, with steel, aluminum, and downstream products facing some of the steepest tariffs in recent history. For manufacturers and importers, these changes redefine sourcing strategies, compliance requirements, and supply chain resilience.

In June 2025, the U.S. government doubled down on tariffs for steel and aluminum imports under Section 232 of the Trade Expansion Act. Section 232 gives the president the authority to impose tariffs or other trade restrictions on imports if the U.S. Department of Commerce determines that those imports threaten national security. Since 2018, these imports have been subject to a 25% duty, but the new policy has raised that figure to 50% for most countries.

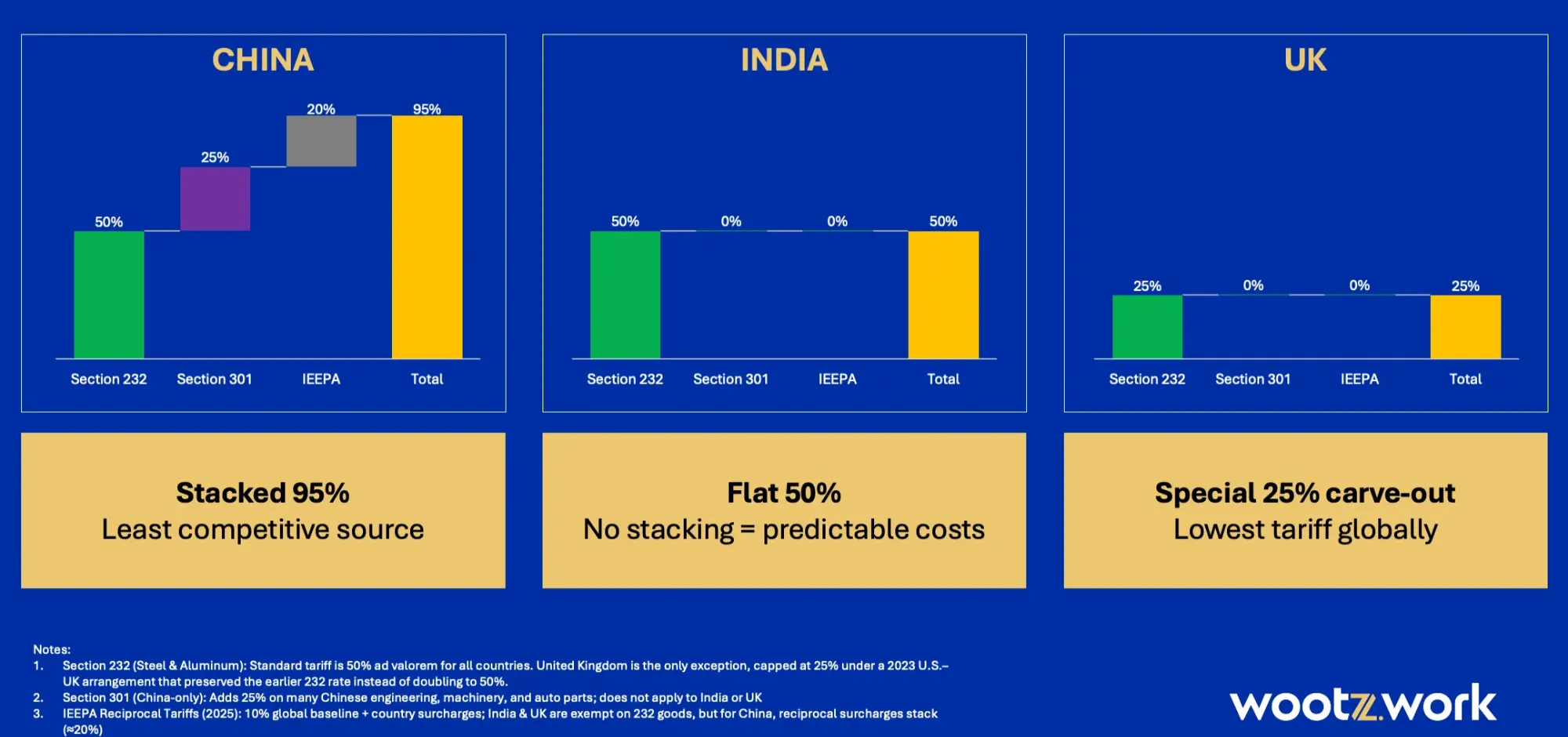

Section 301 tariffs are applied mostly to Chinese goods as a penalty for unfair trade practices, and these stack on top of section 232, making China the most expensive source today with upto 95% duty. India’s tariffs are now at 50% with no additional stacking, keeping the tariffs stable. The United Kingdom remains an exception, having secured a negotiated cap of 25%, the lowest tariff rate available globally for these materials.

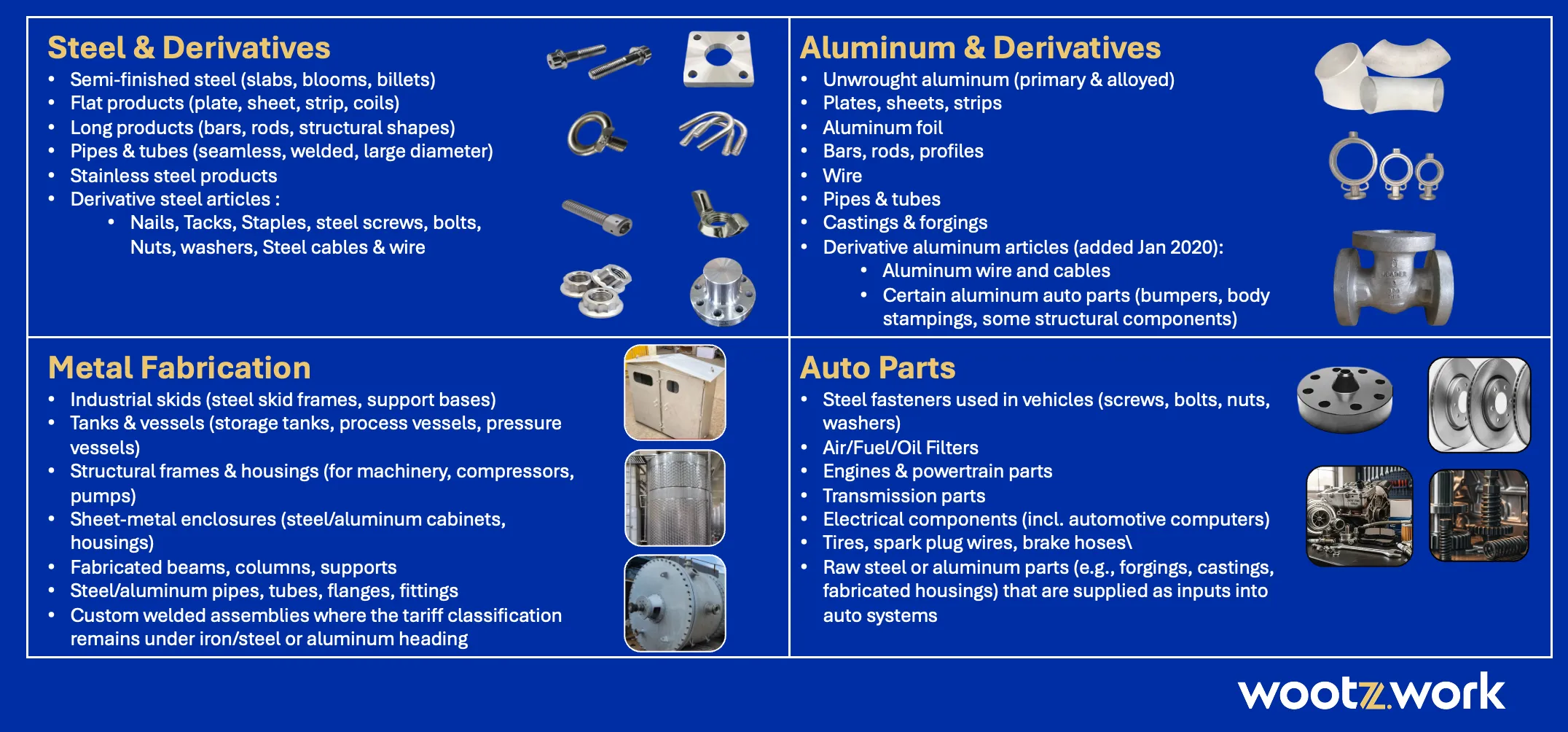

This shift is not only about raw steel and aluminum. In August 2025, the scope of Section 232 was widened to include over 407 new tariff codes to cover “derivative” products, goods that incorporate steel or aluminum but were not previously subject to these duties. Copper products were also brought into Section 232, now carrying a 50% tariff rate for most countries. This change has dramatically broadened the tariff net, reshaping the cost base for many U.S. manufacturers and importers.

Under the updated rules, the duty applies only to the metal content of these derivative goods, with non-metal components taxed separately. That means importers now need to calculate and declare material breakdowns far more precisely than before.

An important change that happened in 2025 was the termination of long-standing exemptions and quotas.

Previously, major trading partners such as Canada, Mexico, the EU, Japan, South Korea, Brazil, and Australia had negotiated carve-outs, quota arrangements, or partial exemptions. These were eliminated under the new tariff proclamations. Their exports to the U.S. now face the full 25% (aluminum) or 50% (steel) tariff rates.

The expansion of Section 232 in mid-2025 has direct, material consequences for anyone sourcing steel, aluminum, or fabricated parts into the United States.

1. Higher baseline costs

Originally introduced in 2018 at 25%, Section 232 tariffs were intended to protect the U.S. steel and aluminum industries on “national security” grounds.

By June 2025, that baseline doubled to 50% for nearly all countries, instantly raising the cost of imported raw materials and components. For China, the picture is even harsher: Section 232 stacks on top of Section 301 tariffs (trade remedies for IP theft and unfair practices) plus reciprocal duties imposed under IEEPA, bringing effective rates close to 95%.

While India’s exports face the same 50% tariff as most countries, they are not hit by Section 301 or reciprocal duties. For U.S. buyers, this means fewer risks of sudden reclassification or hidden tariff shocks.

2. Wider product coverage

In August 2025, the US government has added 407 new Harmonized Tariff Schedule (HTS) tariff codes under Section 232, which pulls derivative products into scope. These aren’t just for flat steel sheets or aluminum bars anymore. They also include the fabricated and engineered products that make up day-to-day industrial supply chains.

3. Classification and compliance challenges

Because duties are levied only on the steel or aluminum content, importers now need precise material breakdowns in customs filings. For example, a pump housing that is 70% steel and 30% polymer will have the tariff applied only to the steel share of its value. Without accurate declarations, shipments risk being misclassified, overcharged, or delayed at the border.

4. Supply chain uncertainty

For importers, the uncertainty is two-fold. On one side, tariff exposure directly changes the total cost calculations and can erode margin mid-project. On the other hand, the compliance and documentation requirements add friction to lead times. Customs audits, re-work requests, and potential penalties are more likely under the new regime.

5. Strategic sourcing pressure

Ultimately, the tariffs are forcing U.S. manufacturers to rethink where they source from. The choice of country now decides cost stability: predictable 50% from India, capped 25% from the UK, or volatile 95%+ from China. Buyers who fail to adjust risk being priced out by competitors who build tariff-resilient sourcing strategies.

Manufacturers and importers cannot afford to treat these tariffs as background noise. The best first step is to audit your portfolio of imports. Every SKU should be reviewed for possible exposure to the expanded list of Section 232 derivative codes.

Once exposure is identified, businesses need to engage with suppliers more actively.

These questions now matter as much as price and quality. Being clear on these answers will help safeguard against sudden cost escalations and strengthen supply chain predictability under the new tariff regime. Strategic sourcing will also play a larger role. Many U.S. buyers are already reconsidering supply footprints, shifting critical parts to countries where tariffs are capped or predictable. Locking in tariff-inclusive quotes is becoming essential to avoid cost shocks mid-project. It also helps build safety stock or diversify sources to cushion against unexpected customs delays.

At Wootz.work, we anticipated these shifts and designed our manufacturing model to help U.S. buyers adapt. We give importers tariff-resilient sourcing options and can shift production to where it makes the most sense. We help you weigh different lead times and compare them against the total cost to keep sourcing predictable, cost-effective, and stable, no matter how tariffs move. Our expertise covers exactly the kinds of derivative products most affected by the August expansion: fabrications, fasteners, skids, tanks, frames, housings, and welded assemblies. We provide “tariff-baked” final-cost quotes so buyers see the full financial picture up front: duties, freight, and compliance included. Every order comes with complete documentation, including ASME, ISO, and BPCV certifications, along with traceability for metal content. That means smoother customs clearance, fewer surprises, and a stronger foundation for long-term cost predictability.

Disclaimer: The information in this presentation is based on Wootzwork’s independent analysis of public sources, government announcements, and our own export experience. While we strive for accuracy, tariff regimes are volatile and subject to frequent revision or reinterpretation by authorities in the United States, India, the United Kingdom, and the European Union. This article is provided solely for informational purposes. It does not constitute legal, tax, customs, or compliance advice in any jurisdiction. The views expressed are those of Wootzwork Labs Pvt. Ltd. (India), Wootzwork Labs Ltd. (UK), and Wootzwork Labs Inc. (U.S.), and may not reflect official government positions. Stakeholders are encouraged to consult qualified legal, trade, or customs advisors, as well as official government publications, before acting on this information. Wootzwork disclaims any liability for losses, costs, or damages arising from reliance on this material.

.svg)